Bridge and tunnel projects carry long tails. A contractor mobilizes heavy equipment, secures staging areas, opens cofferdams, orders steel and precast, and starts pouring concrete. Millions are at risk well before the first pier rises out of the river or a TBM bites into soil. Owners cannot afford to hope the contractor finishes. They need a mechanism that turns a paper contract into a completed structure, even if things go wrong. That mechanism is the performance bond.

The core idea, plain and simple

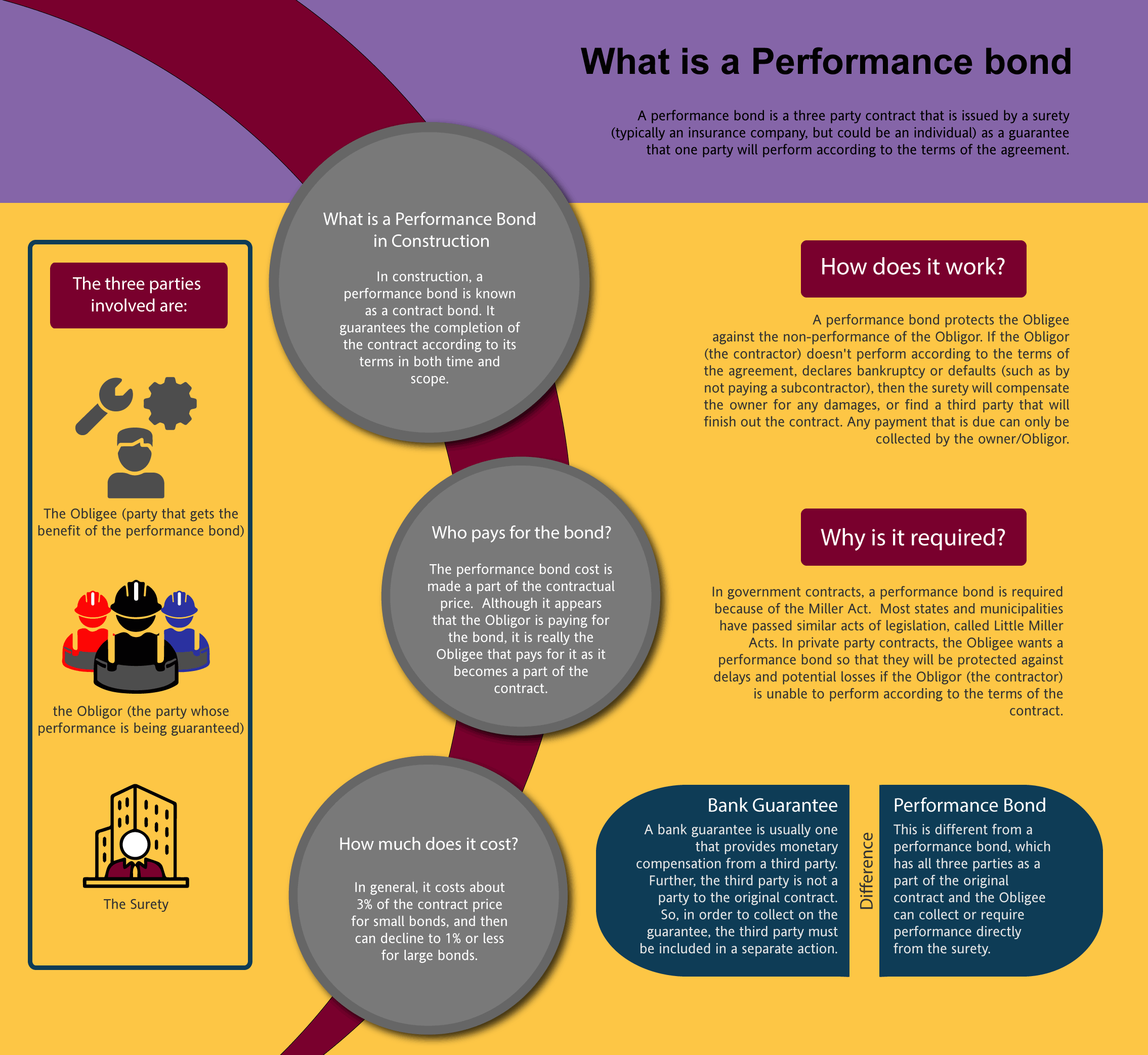

If you have ever asked, what is a performance bond, think of it as a promise backed by a third party. A surety company, usually an insurance-affiliated entity with strong financial ratings, guarantees that the contractor will perform the construction contract in accordance with its terms. If the contractor defaults, the surety steps in, within the bond’s penal sum, to ensure completion or compensate the owner for the cost to complete.

The bond is not insurance in the usual sense. The surety expects to be repaid by the contractor for any losses. That expectation drives everything from prequalification to the structure of the bond form. For bridges and tunnels, where individual change orders can run into seven figures and geotechnical surprises can flip a schedule overnight, that discipline becomes critical.

Why bridges and tunnels need more than generic protection

A low-rise commercial build can often be salvaged by swapping a subcontractor or accelerating finishes. Subsurface structures and long-span bridges do not lend themselves to quick fixes. Complexity stacks up:

- Large mobilization and specialized methods: cofferdams, marine access, segmental casting, TBMs, NATM sequences, ground freezing, jet grouting. Interfaces with public safety and operations: railroad corridors, navigable waterways, high-traffic arterials. Irreversibility of partially completed work: once a shield pass starts, stopping mid-drive risks settlement or flooding; once tendons are stressed, access for correction is limited.

Those realities raise the stakes of contractor failure. A half-built arch over a river is not just an eyesore, it is a navigational hazard. A stalled tunnel face can destabilize blocks of a city. Owners, from state DOTs to port authorities, rely on performance bonds to keep projects moving if the prime contractor falters.

How a performance bond is structured

A typical performance bond ties three parties together:

- The principal: the contractor obligated to perform the work. The obligee: the project owner who benefits from the bond. The surety: the company that promises to step in if the principal defaults.

The bond amount, called the penal sum, is usually 100 percent of the contract price for public infrastructure in the United States, and often similar in Canada and many other jurisdictions. On a 220 million dollar bridge replacement, the penal sum equals 220 million dollars at award, then adjusts with change orders. Some owners accept lower amounts for preconstruction services or design-build phases when the scope is developing, then require an increase once work becomes fixed and field activity begins.

The bond references the construction contract and incorporates it by reference. That means every drawing, spec, addendum, and executed change order defines what the surety is backing. It also means sloppy scoping can undermine recovery. In my experience, the best bond is only as good as the clarity and enforceability of the underlying contract documents.

Triggers and remedies: what happens if trouble hits

A performance bond is not a blank check. The owner must declare the contractor in default under the contract, satisfy any notice and cure provisions, and formally make a claim on buy swift bonds the bond. Well-drafted contracts require clear written notices and a chance for the contractor to cure within a defined period, commonly 7 to 30 days depending on the severity.

Once the surety receives a proper declaration of default and claim, it typically investigates quickly. On large civil work, most experienced sureties will engage independent engineers to understand status, percent complete by cost code, critical risks, long-lead items, and the burn rate. Time is nearly always the enemy. The bond’s real value is measured in how fast the surety can put structure back into a failing job.

Sureties generally have several options, sometimes enumerated right in the bond form or the contract:

- Finance the existing contractor so it can finish, often with oversight and strict controls. Tender a completion contractor that the owner can accept or reject, then pay the differential up to the penal sum. Take over the contract and manage completion itself through a selected builder. Pay the owner the cost of completion, again limited by the penal sum, and let the owner procure completion directly.

Each path has trade-offs. Financing a struggling contractor can be fastest if the cause of distress is temporary, such as a cash crunch or a problematic subcontractor. Tendering a replacement can reduce risk but usually adds delay and mobilization costs. Takeover gives the surety more control but can strain relationships with the owner. A pay-and-walk approach puts risk back on the owner to manage completion.

On a river bridge I worked on fifteen years ago, the prime fell into a liquidity crisis halfway through pier construction. The surety chose to finance completion with strict milestone-based funding and independent cost-to-complete monitoring. That decision saved a season on the water, which mattered more than wringing out every dollar of recovery. The bond’s flexibility, used with judgment, kept the navigation channel free and avoided two winters of delay.

How sureties underwrite heavy civil risks

Sureties are conservative by nature. For a major bridge or tunnel, underwriting digs into three buckets:

- Contractor capacity: past performance on similar scope, working capital, net worth, backlog relative to capacity, and management bench depth. A firm that has built six steel plate girder bridges may not be ready for a 1,200-foot cable-stayed structure with complex stay anchorages. Project risk profile: geotechnical variability, environmental permits, railroad or maritime coordination, utility conflicts, constructability of the chosen method, and schedule realism. Tunnels under rivers with mixed face conditions and high groundwater draw the most scrutiny. Contract terms: risk allocation for differing site conditions, design responsibility in design-build, liquidated damages, force majeure clauses, escalation provisions, and dispute resolution steps.

On a cut-and-cover urban tunnel, for example, an owner who rejects any differing site condition clause pushes subsurface risk entirely onto the contractor. Many sureties either price that risk through premium and collateral requirements, or they decline to write the bond unless the risk is moderated. It is not personal, it is arithmetic. The expected value of potential loss must fit within the contractor’s balance sheet and the surety’s appetite.

Interplay with payment bonds and subcontractors

Performance bonds often sit beside payment bonds, which guarantee that laborers and material suppliers get paid. The two are related but distinct. The performance bond protects the owner’s completion interest, while the payment bond shields against liens and keeps the supply chain flowing. On bridges and tunnels, where reinforcing steel, PT cables, segment molds, precast liners, and specialized subcontractors are critical path, a robust payment bond can prevent a cascade of disruptions.

Subcontractor default insurance (SDI) sometimes replaces or supplements individual sub bonds. On a segmental bridge job where a single formwork supplier had production issues, SDI enabled the prime to bring in a second vendor quickly, while the performance bond stood back because the prime remained capable of completing the work. Owners rarely see SDI directly, but they benefit when primes use it to stabilize subs and suppliers, especially on long fabrication chains.

Design-build, P3, and how delivery model changes the bond

Not all performance bonds look the same across delivery methods:

- Design-bid-build: the classic model. The contractor builds the owner’s design. The performance bond backs construction only. Errors in owner design are not the contractor’s risk, though coordination and means and methods remain the contractor’s responsibility. Design-build: the contractor carries design responsibility. The performance bond covers design and construction obligations. Sureties look closely at the design team’s credentials and the interfaces between design packages and field production. Public-private partnerships (P3): the project company, or concessionaire, is responsible for design, build, finance, operate, and maintain for decades. Lenders often require a large EPC wrap and bonding on the EPC contract. The bond might be complemented by parent company guarantees, letters of credit, and step-in rights. For a tunnel with 30-year operations, O&M performance security may take forms other than a traditional construction performance bond, such as long-term maintenance bonds or performance letters of credit.

In Canada and parts of Europe, bonding norms in P3s can involve layered arrangements, including performance bonds for key subcontractors like segment manufacturers or M&E integrators. The logic is simple: spread performance security across the nodes where a single failure could shut the whole system.

The numbers that matter: penal sum, delay costs, and practical caps

A 100 percent performance bond does not mean the surety will cover every conceivable cost overrun. The penal sum caps liability, and it includes amounts the surety pays for any option it chooses. On a 400 million dollar immersed tube tunnel segment, if default occurs at 60 percent complete and the cost to complete is 220 million dollars instead of the 160 million dollars left in the original contract, the gap is 60 million dollars. If the penal sum has been eroded by prior surety expenditures, such as financing or temporary works, the available cushion shrinks.

Delay damages can be contentious. Some bond forms explicitly exclude consequential damages but allow recovery of liquidated damages if they are part of the contract and directly tied to completion. Owners that need certainty should align the bond form with the contract’s damage regime and avoid mismatches. I have seen disputes where the contract allowed for liquidated damages of 200,000 dollars per day on a tunnel portal, but the bond form limited the surety’s exposure to direct costs to complete, not time-related damages. That gap made negotiations slower and more strained than they needed to be.

Claims, investigations, and keeping the site safe

Once default is declared, immediate priorities are safety, environmental compliance, and asset protection. A bond does not suspend the need to maintain cofferdams, dewater shafts, or shore excavations. Most sureties will fund interim stabilization while they assess options. Owners help themselves by preserving records: daily reports, photos, as-built surveys, certified payrolls, and submittal logs. The speed at which the surety can make an informed decision depends on the clarity of this documentation.

One winter on a mountain highway bridge, the contractor ran out of cash with two piers partly poured. The lake level was rising and snowmelt threatened the work. The surety authorized emergency measures within a week: winter protection, supplemental pumping, and ice booms near temporary trestles. That spend came out of the penal sum, but it prevented weeks of demolition later. The takeaway is clear: early, targeted stabilization often saves multiples down the line.

Common pitfalls that blunt a bond’s value

From the owner side, three patterns recur:

- Sloppy default process: skipping notice or cure periods can give the surety a procedural defense. Follow the contract. Put it in writing. Keep a timeline. Scope drift without change orders: field directives and handshake deals that never become executed change orders create ambiguity. If a surety cannot tie costs to an approved scope, negotiations stall. Incomplete record of progress: without a current schedule, earned value, and updated quantities, determining percent complete becomes guesswork. Owners should require monthly cost-loaded schedules and quantity books from day one.

From the contractor side, pitfalls look different:

- Underestimating geotechnical complexity: optimism bias on rock quality, groundwater inflows, or soil behavior shows up later as claims and schedule slippage. Sureties discount confidence without data. Overextended backlog: winning three major jobs is not capacity if the same project manager is named on all three. Sureties look for real people, not resumes recycled across proposals. Poor subcontractor vetting: a TBM supplier missing factory acceptance milestones or a segment plant with QC issues can sink margins and schedules. The prime remains on the hook. Sureties like to see thorough prequalification write-ups for critical trades.

How performance bonds interact with risk allocation

A bond is not a substitute for balanced risk allocation. It sits on top of whatever the contract assigns. If a design-build tunnel puts all geotechnical risk on the contractor with limited data and no escrowed geotechnical baseline report, the surety will price that or step back. Conversely, if the owner provides a solid baseline report, clearly defines compensation events, and sets a reasonable escalation mechanism for steel and cement, bond availability and cost improve.

On large bridges, wind engineering and aerodynamic stability of the superstructure can be a hidden risk. If the design team commits to a particular girder profile but the wind tunnel shows instability late in design, redesign and fabrication changes can be brutal. Tying that risk to design responsibility, with appropriate contingencies, helps keep the bond’s role clean: cover the obligation to deliver the design-conforming product, not to eat owner-initiated redesigns.

Premiums, collateral, and what it costs

Performance bond premiums on heavy civil work often fall in the 0.5 to 1.5 percent range of the contract value for the base term, sometimes less for very large jobs with strong contractors. Rates depend on project duration, complexity, the contractor’s financials, and the surety relationship. On a 300 million dollar bridge with a four-year duration, a 1 percent premium means around 3 million dollars paid over the life of the job, often in installments that track progress.

Collateral is not typical for strong contractors with clean financials, but sureties may require letters of credit or pledged assets if the contractor’s working capital is thin or the project risk is unusual. Expect more stringent terms if the job includes long fabrication with high cancellation penalties or a geology profile with major unknowns.

Practical steps for owners to make the bond work for them

A few habits from the owner’s side multiply the effectiveness of performance bonds:

- Choose a bond form you have used successfully and that courts recognize. Industry forms from AIA or consensus documents work, but modify carefully. Overreaching exclusions can make experienced sureties walk. Align the bond with the contract. If the contract imposes liquidated damages, ensure the bond does not exclude them. If you need the surety to respond quickly, write response timelines into the bond. Prequalify the contractor with a focus on relevant experience. Ask for evidence of bonding capacity on similar projects and commitment letters from sureties early, not at award. Maintain disciplined documentation. Require monthly cost-loaded schedules, updated risk registers, and field reports. If a default occurs, you will need this to quantify completion costs.

On a tunnel ventilation upgrade where access windows were narrow, the owner required two independent schedules: an activity logic schedule and a vent-outage schedule tied to operations. That might seem fussy until disruption risk hit. When the contractor stumbled, those schedules let the surety and owner plug a new team in with minimal friction, because both the work sequence and the operational windows were crystal clear.

What contractors can do to secure and keep bonding

Contractors sometimes view sureties as gatekeepers. The most successful firms treat them as financial partners who prevent taking on more than the balance sheet can support. Practical moves include:

- Keep financial statements current, audited, and conservative. Bonding is built on trust in numbers. Invest in project controls. Earned value, risk registers, change management logs, and accurate cost-to-complete forecasts reduce surprises that make sureties nervous. Build a record of like-for-like delivery. If you are leaping from short-span steel to a cable-stayed main span or from microtunneling to a large pressurized TBM, bring in joint venture partners with the missing skills and make sure the operating agreement gives them real roles. Manage claims professionally. Differences over changed conditions or owner directives happen. Timely, well-supported notices maintain credibility with both the owner and the surety.

A contractor I worked with moved from mid-range highway bridges into segmental construction by forming a JV with a European firm known for long viaducts. The surety initially capped their single-job program at 150 million dollars. After two years and clean delivery on a 180 million dollar viaduct, the cap rose to 400 million dollars. Capability breeds capacity.

International flavors and local nuances

Bonding norms vary. In the United Kingdom, performance security often takes the form of on-demand bonds or performance letters of credit at 10 percent of contract value, reducing over time. In parts of Asia and the Middle East, on-demand bonds are common and can be called without proving default, which materially changes contractor risk and pricing. Civil-law jurisdictions may mandate different notice procedures or offer fewer defenses for sureties.

In the United States, federal projects fall under the Miller Act, which requires performance and payment bonds on most federal construction contracts above a threshold. State “Little Miller Acts” mirror these requirements. That statutory backdrop makes bonding a near-universal feature of public bridges and tunnels in the U.S. Private owners sometimes mimic the regime when projects interface with critical public infrastructure.

Edge cases: when a performance bond is not the right tool

Not every risk fits neatly into a performance bond. Manufacturing long-lead bespoke equipment, like a TBM, may be better secured with parent guarantees and progress-linked letters of credit payable on missed milestones. Long-term operations obligations in P3s often rely on performance guarantees and reserve accounts rather than classic construction bonds. For highly specialized design work, professional liability insurance, not a performance bond, addresses design error and omission risk.

There are also times when owners intentionally accept reduced bonding in exchange for price or innovation, especially with early contractor involvement. If you go that route, set clear gates: limited notice to proceed for preconstruction at a smaller bond value, with the bond increasing once design risks settle and construction begins.

A brief case study: bonding in a live-traffic tunnel rehab

A metropolitan agency needed to replace fire standpipes, lighting, and ventilation controls in a 1950s-era tunnel with only short nightly closures allowed. The contractor’s plan hinged on prefabricated racks and plug-and-play connections to cut outage time. Midway through, supplier delays stacked up. Schedule float evaporated, and missed outages began to trip liquidated damages.

The agency issued a cure notice under the contract. The contractor acknowledged the slippage but argued for compensable time due to added work. The surety monitored quietly at first, then facilitated a meeting where the parties agreed to a recovery schedule and a re-sequenced outage plan. The surety provided limited financing for the supplier to ramp production and insisted on a weekly look-ahead schedule tied to outage access.

The job finished three months later than the original date but within the revised recovery plan. The bond was never formally called, yet its presence changed behavior. With the surety in the room, the contractor tightened controls, the owner made quicker decisions on access, and the supplier received bridge financing pinned to measurable outputs. That is a soft success, but a real one. A good bond presence does not always show up as a claim payment. It often shows up as discipline that prevents the cliff.

Final thoughts from the field

The best time to think about a performance bond for a bridge or tunnel is when the project is still a stack of drawings and borings, not when cranes are already on site. Owners control two levers that matter most: write a balanced, clear contract and select teams with the right experience. Contractors control two more: keep your financial house in order and be honest about capacity.

A performance bond cannot turn poor planning into a good outcome. What it can do is keep a complicated project from collapsing when something material goes wrong. It gives the owner leverage, time, and a funded path to completion. In the world of long spans and deep excavations, that is not a luxury. It is part of the foundation.